.svg)

.svg)

Bank Payments Has Always Had a Built-In Safety Net

That Cushion is Disappearing

For decades, bank payments had something that nobody talked about as a risk management tool, because nobody had to: time.

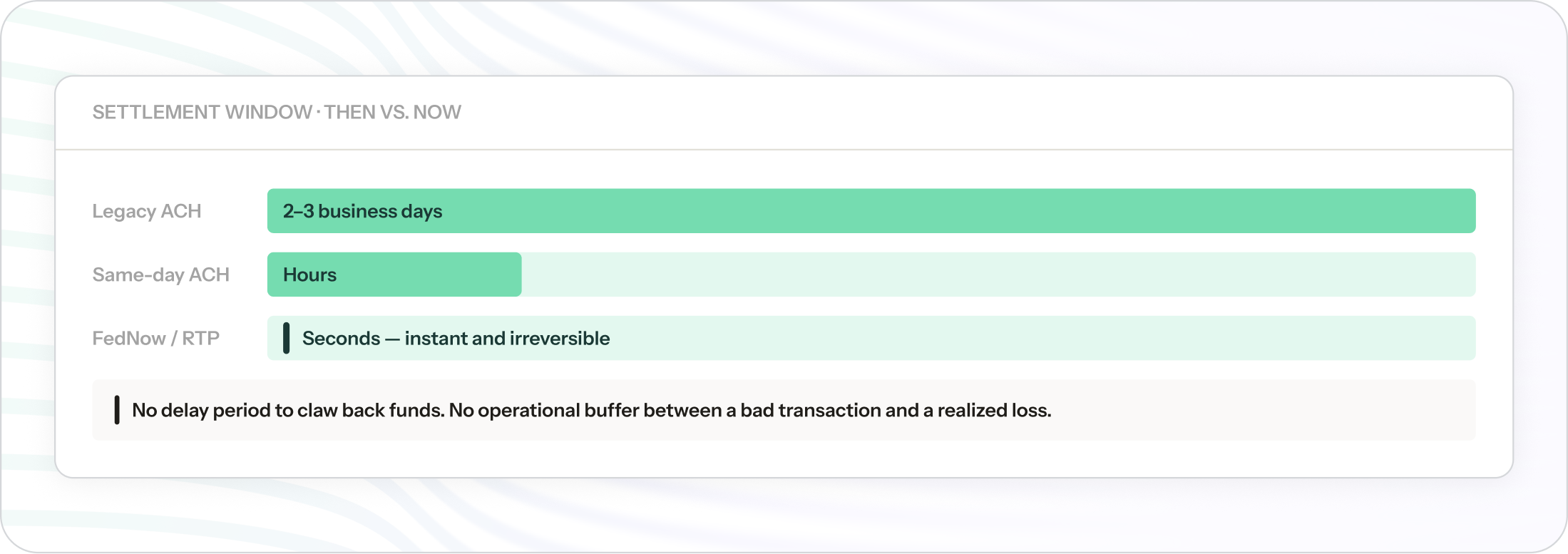

ACH is designed around batch processing. Transactions are collected, submitted, and settled over a multi-day cycle. If something went wrong, like an invalid account, an unauthorized debit, or a fraudulent actor, there was a recoverable period where failures surfaced and operations teams could intervene. Returns came back. Disputes were filed. Manual reviews rightsized things.

The system was slow, but the lack of speed was load-bearing. It gave businesses and financial institutions room to catch problems before they became losses.

That era is ending.

Same-day ACH compresses the timeline but still operates within the window-based framework. Real-time payment rails like FedNow and RTP eliminate it entirely. These transactions are instant and irreversible. No delay period to claw back funds, and no operational buffer between a bad transaction and a realized loss.

Real-time rails are only the beginning. Agentic commerce, where AI agents initiate, negotiate, and execute payments on behalf of businesses and consumers will introduce transaction volumes and velocities that no human-in-the-loop process can govern. Stablecoins are enabling an entirely new class of programmable payment rails, built from scratch, where the infrastructure for trust and identity has to be baked in from the start rather than retrofitted onto legacy systems.

All of these developments point in the same direction: the standard for preemptive risk management needs to be dramatically higher than anything that has historically been available.

Not incrementally better. Structurally stepped up by design.

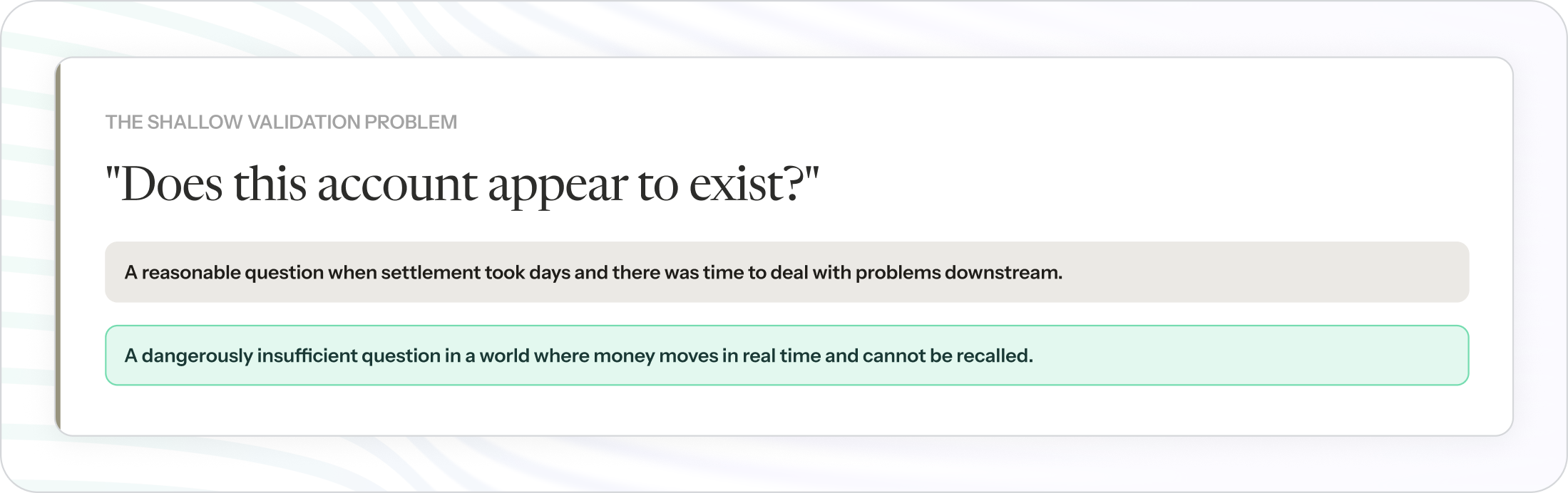

The Shallow Validation Problem

The bank payments industry has not been standing still. There are tools available for validating accounts, checking credentials, and screening transactions. But the vast majority of what’s on the market today operates on what amounts to shallow validation; a narrow set of data points, checked once, with no memory and no ability to build on what was learned to reuse elsewhere.

Micro-deposits confirm that an account can receive a transaction. They take days to complete, create friction for end users, and tell you almost nothing about the account’s history, ownership confidence, or risk profile. Account number lookups verify formatting and basic routing information. One-time credential checks confirm that a user presented valid information at a specific moment, then shelve the insights.

These tools answer a simple question: does this account appear to exist? That was a reasonable question when settlement took days and there was time to deal with problems downstream. It is a dangerously insufficient question in a world where money will move in real time and cannot be recalled.

The deeper issue is that shallow validation wastes what could be valuable signal. Every account verification interaction generates data; about the account, the entity behind it, the context of the request, and the behavioral patterns at play. Legacy providers check a box and throw that signal away. Even when they get the answer right in the moment, they start from zero the next time they see the same account, the same entity, or a similar pattern. The result is an industry that generates enormous amounts of risk-relevant data at the point of validation, then systematically fails to use it.

What Changes When Validation Gets Richer

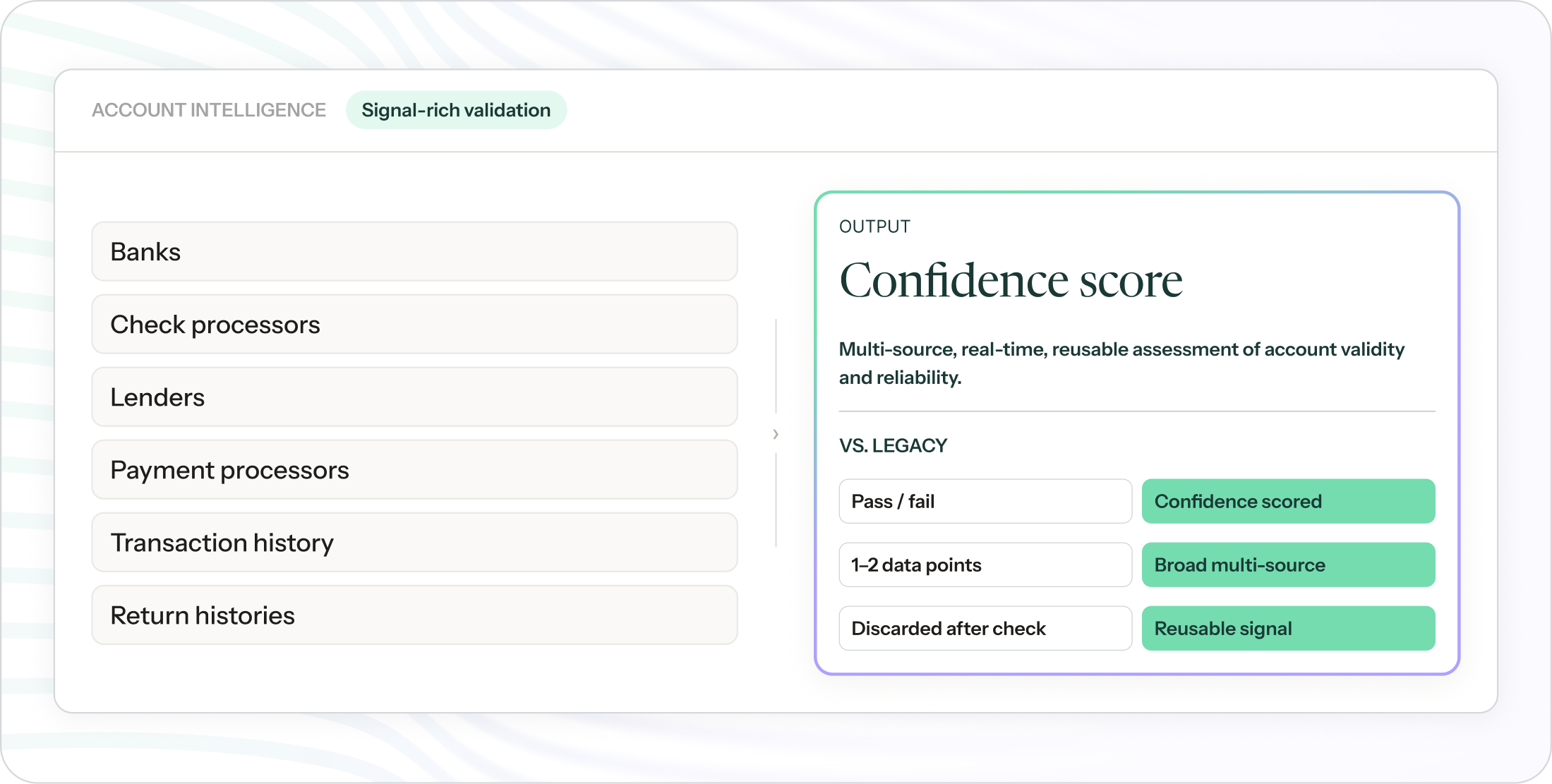

GrailPay’s Account Intelligence represents a fundamentally enriched approach to bank account validation. Rather than checking one or two data points and returning a binary pass/fail, Account Intelligence aggregates data across a broad set of sources; banks, check processors, lenders, payment processors, and more, and assesses historical transaction patterns, return histories, and advanced risk scoring models to deliver a confidence-scored assessment of an account’s validity and reliability.

This is a massive step up from legacy validation. The coverage of accounts is broader. The signal on every check is rich and actionable. The decisioning happens in real time and is reusable.

For businesses running bank payment programs today, it represents the best available front-line defense against failed payments, unauthorized transactions, and onboarding friction.

But here’s what we’ll say plainly: even best-in-class validation at the point of account onboarding is the floor, not the ceiling. It is the bare minimum for what’s required as payment rails get faster and more complex.

A strong initial validation is necessary now, but not sufficient for the future of commerce.

The reason is straightforward. Validation happens once. Risk is continuous. An account that looks clean today can be compromised tomorrow. A pattern of behavior that seems normal in isolation looks suspicious in a broader context of payment velocity changes, counterparty history updates, and network-wide signals. Single-point-in-time assessment, no matter how thorough, cannot account for what happens after the check is done.

What GrailPay’s signal-rich validation does provide is the foundation for something more powerful.

When your initial assessment generates deep, multi-source intelligence about an account, that intelligence becomes the raw material for continuous monitoring, behavioral analysis, and persistent identity when built on an intelligent architecture specifically designed to retain it, build on it, and ultimately share it.

Validation to Monitoring to Persistent Trust

GrailPay’s risk intelligence architecture is designed as a cumulative system where each layer builds on the signal generated by the layer beneath it.

Account Intelligence establishes the foundation. It delivers signal-rich validation at the point of account onboarding, confirming not just that an account exists, but how much confidence you should have in it, informed by historical data, cross-source verification, and predictive risk scoring. This is where the painting of a holistic picture of risk data begins.

Transaction Intelligence adds continuous behavioral monitoring on top of that foundation. Rather than assessing an account once and moving on, Transaction Intelligence evaluates every payment interaction against behavioral attributes, timing patterns, amount thresholds, identity factors, and historical outcomes. It transforms a single data point into an evolving risk picture that gets sharper with each transaction.

Together, these products generate a depth of intelligence that shallow validation providers simply cannot match. But without a connective layer to retain that intelligence, make it portable, and compound it over time, each assessment still starts closer to zero than it should.

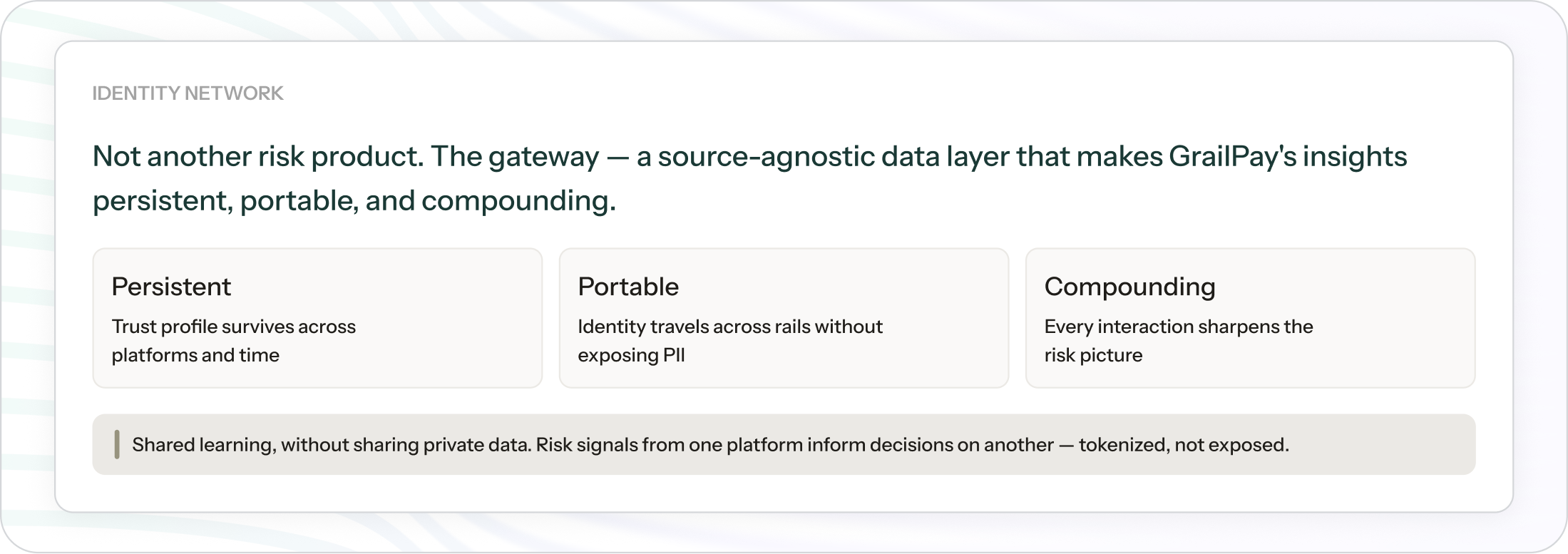

The Identity Network: A Persistent Layer Across GrailPay's Risk Intelligence

This is where the GrailPay Payments Identity Network comes in, and it’s important to understand what it is and what it isn’t.

The Identity Network is not another risk or compliance product. It is the gateway; a source-agnostic data layer that wraps GrailPay’s risk platform and makes its insights persistent, portable, and compounding.

When a user or business authenticates through the Identity Network, a secure, tokenized payment identity is generated. That identity binds the entity to its payment behavior across platforms and rails without exposing sensitive data. Every interaction - every validation, every transaction assessment, every outcome - feeds into the identity’s trust profile. Trust accumulates through positive outcomes. Confidence decays and alerts arise when risk signals emerge. The identity persists across use by different authenticated platforms, learns from every touchpoint, and reduces friction for trusted entities while escalating scrutiny only when warranted.

The practical effect is that platforms using GrailPay no longer force every user through the same level of friction regardless of history. A counterparty with hundreds of clean settlements doesn’t get treated like an unknown entity every time they interact with a new platform. And a new account exhibiting patterns that the network has learned to associate with risk gets flagged before damage is done.

Critically, this works across the network without sharing personally identifiable information between participants. Risk signals observed on one platform inform decisions on another. Shared learning, without sharing private data.

Current Standards Aren’t Ready

The shift from batch ACH to real-time rails is significant, but it’s only the first wave. Two additional forces are converging that will demand an entirely new standard for payment trust infrastructure.

Agentic commerce will require risk systems that are rule-based, preemptive, auditable, and portable. When an AI agent initiates a payment, a single pass/fail check is not sufficient. Every check in a compounding series of validations needs to succeed all together. What happened at each stage; what information was authenticated, what signal was returned assessed, and what was flagged needs to be fully documented and auditable. And because agentic commerce can happen everywhere at once, across platforms and counterparties simultaneously, that audit trail and trust profile needs to exist across the identity and update autonomously at the speed of the agents using the network.

A system that only works within one platform’s walls cannot govern transactions that by nature span many.

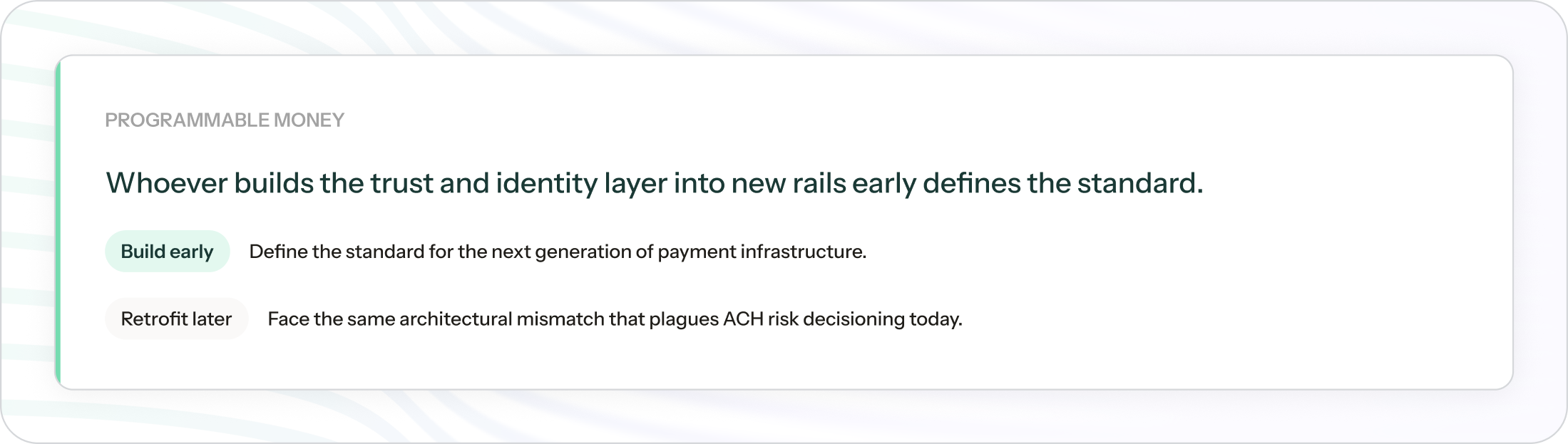

Programmable money represents something even more fundamental. We are watching entirely new payment infrastructure get built from scratch. Whoever builds the trust and identity layer into these rails early defines the standard. Those who try to retrofit legacy validation onto them later will face the same architectural mismatch that plagues ACH risk decisioning today.

The through line across instant settlement, agentic commerce, and programmable money is the same. We’re removing the buffers of built-in delays and humans in the loop. The only acceptable response is preemptive risk decisioning that is richer, continuous, and portable by design.

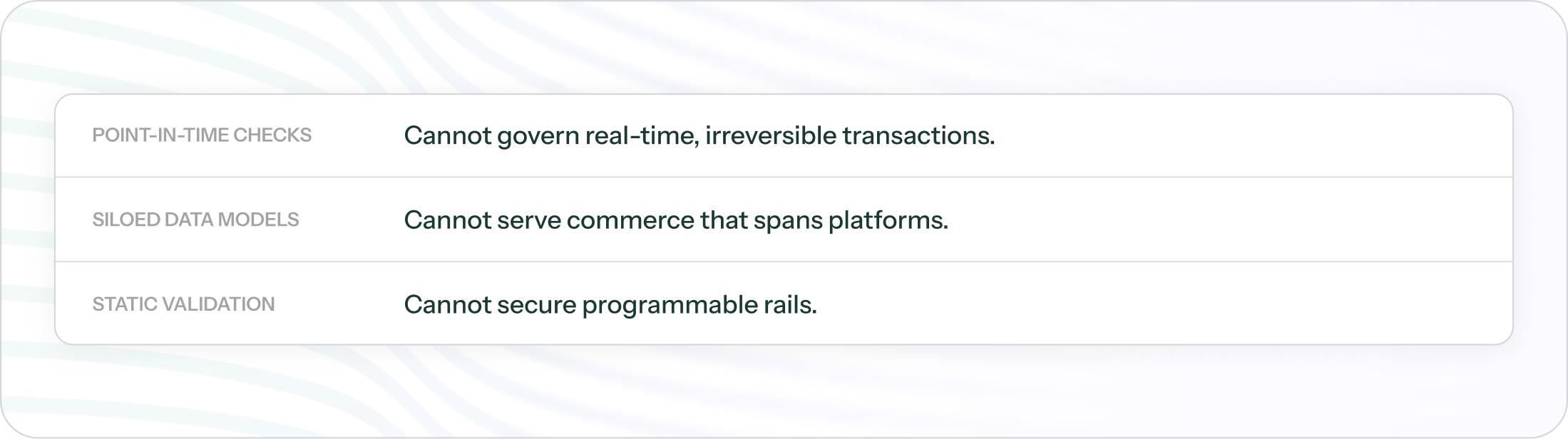

- Point-in-time checks cannot govern real-time, irreversible transactions.

- Siloed data models cannot serve commerce that spans platforms.

- Static validation cannot secure programmable rails.

The Infrastructure Question

The card networks solved this problem for card payments a generation ago. They built shared intelligence, pre-authorization frameworks, and persistent trust systems rooted in household brand names that allowed speed and security to scale together.

Bank payments never got an equivalent. For decades, the slowness of ACH settlement masked this gap. That cover is disappearing.

GrailPay is building the trust infrastructure that bank payments have always lacked, starting with signal-rich validation, extending through continuous transaction monitoring, and delivered through a persistent identity layer that compounds intelligence across every interaction and every platform.

If your current approach to bank payment risk is a vendor that checks an account number and returns a pass/fail, ask a simple question: what happens to everything that check just learned? If the answer is that it’s discarded, and that the next transaction involving that same account starts from zero, on your platform and everywhere else, then you’re not managing risk. You’re just managing the moment.

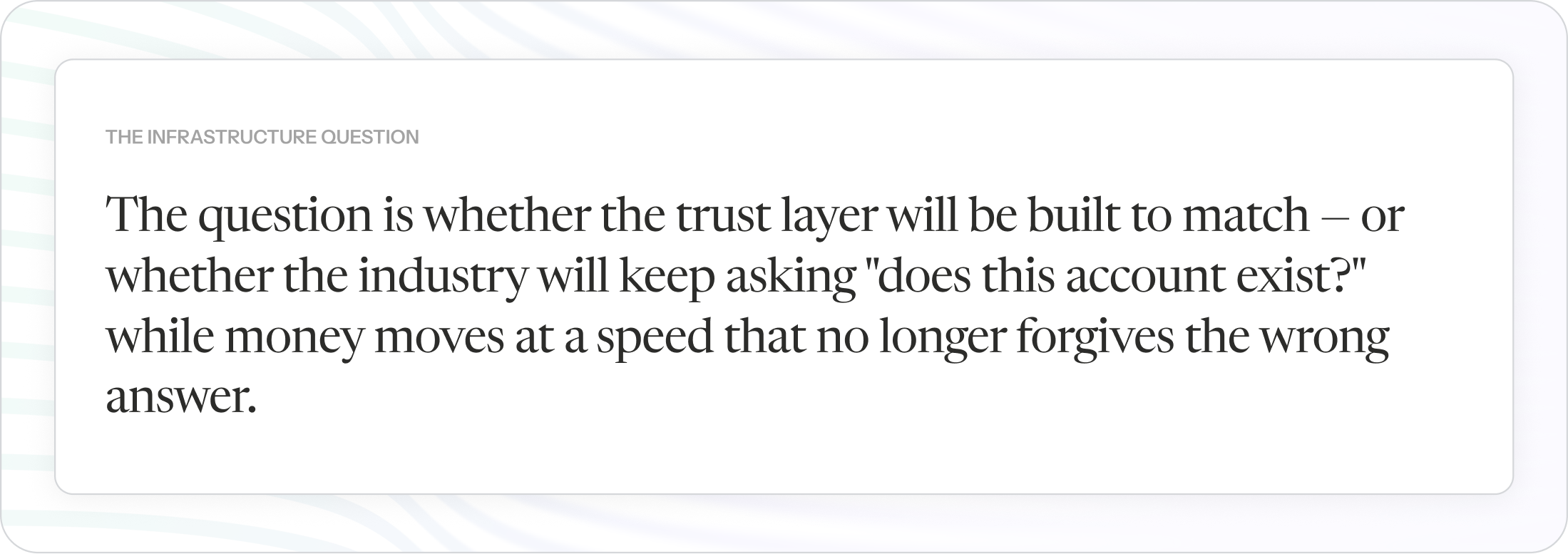

The payments infrastructure of the next decade will be faster, more autonomous, and more programmable than anything that exists today. The question is whether the trust layer underneath it will be built to match, or whether the industry will keep asking does this account exist while money moves at a speed that no longer forgives the wrong answer.

.svg)

.svg)