.svg)

.svg)

Open banking’s uncertain future as the CFPB considers non-enforcement of Rule 1033; banks eye new data fees

Banking juggernaut JP Morgan recently announced that fintechs seeking access to consumer data through open banking connections will now face fees, starting as soon as September 2025. While the exact costs aren’t yet publicly known, leaders at the financial institution have reported positive ongoing discussions with impacted open banking fintechs.

JPMs move might be seen as a natural evolution given the CFPB’s apparent wavering on Rule 1033’s application to consumer privacy rights and access to bank data.

Amidst the turbulence for open banking, other methods of securely authenticating connecting accounts and verifying their details to run bank payments are proliferating. With the advent of AI, data and payment processing companies like GrailPay are accelerating the use of previously untapped datasets to validate bank accounts and monitor transactions, providing a cost effective alternative for fintechs that need to onboard customers and run their payments. End users benefit too with less friction in their bank payment experience; a perfect match in timing as a preference for bank payments continues to grow due to lower fees and increased settlement speeds.

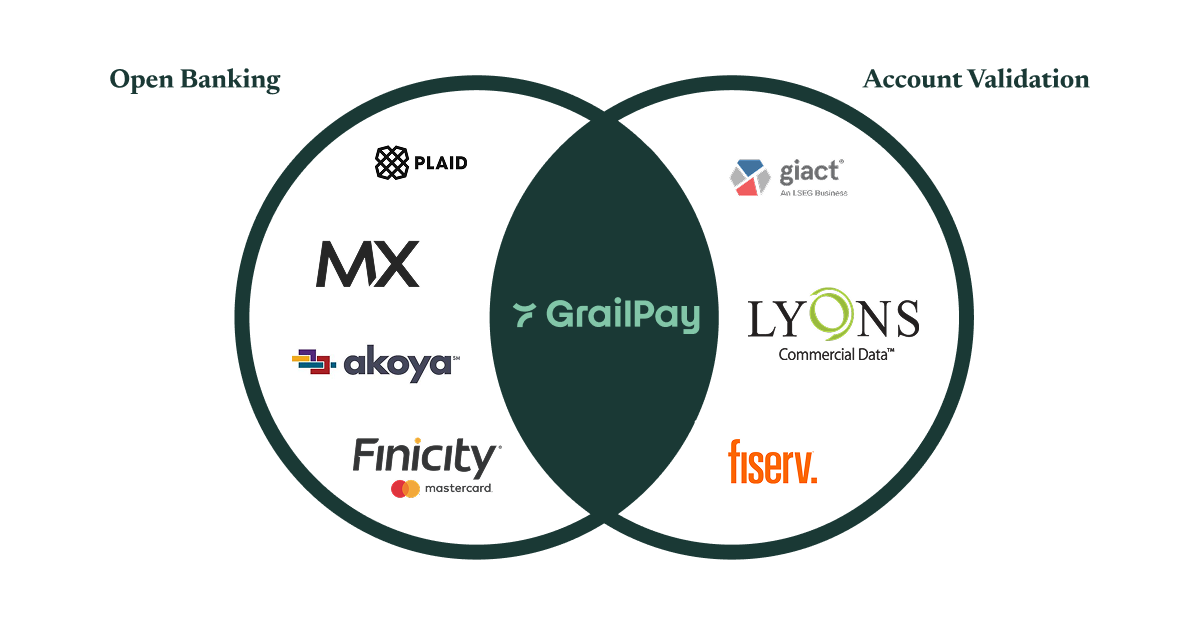

Open banking account connection vs credential-less account validation

When businesses need to connect customer bank accounts for whatever service they offer, two approaches are usually available. Open banking, via aggregators like Plaid, Finicity, MX, and others like them allow individuals to connect their bank accounts through a login interface co-owned by the aggregators and banks that own the accounts being connected. This method provides ongoing access to transaction histories, account balances, and other detailed financial data that can enhance critical risk and payment functions for the fintech providing the service. However, the method can also be high friction, with numerous screens to go through to permission data, and it can suffer from low conversion rates. It is worth noting that the widespread use of open banking aggregators in account onboarding flows indicate that these challenges may be acceptable costs to pay for the quality and reliability of the resulting available data.

Another approach allows for manual entry of account and routing numbers which are then run through validation technology like GrailPay’s Account Intelligence. This method sees an account validation provider run the account and routing numbers through datasets to determine the likelihood of the account credential being real and usable. This method is significantly lower friction, as it focuses specifically on verifying that the provided banking information is legitimate and operational without requiring extensive data access or ongoing account monitoring.

Luckily there are numerous reputable providers for both open banking, and account validation.

Here are some you should know.

A new paradigm for bank data costs and revenue

JP Morgan's decision to charge fintechs for open banking data access represents more than just a new revenue stream. The size and influence of the institution making such a move likely foreshadows a fundamental shift in the economics of financial data; access, use, and commercialization of it.

When one of the largest banks in the country implements fees or makes structural shifts to commercial programs, other financial institutions typically follow suit, shifting industry-wide revenue and costs structures for companies that offer open banking connections, and their customers who build on top.

This development is particularly significant because it arrives at a time when the regulatory landscape around open banking remains uncertain. With the CFPB potentially rescinding the 1033 rule that was designed to standardize open banking practices, companies can no longer count on regulatory pressure to keep data access free or standardized.

The timing offers a curious conundrum for companies that have built payment operations and business models on top of banking integrations. Companies may soon face the prospect of paying multiple fees across different banks while navigating an increasingly fragmented regulatory environment.

Credentialless account validation offers an alternative

Savvy fintech companies are recognizing that not every account onboarding use case requires the full scope of open banking data. For many payment processing scenarios, the core need is simple: verify that a bank account exists, is operational, and belongs to the intended user. This focused approach can achieve the primary goal of reducing payment failures and fraud without incurring the additional, expanding costs and complexities of comprehensive access to user data.

Modern bank account validation solutions aggregate multiple data sources to provide confidence scores on account legitimacy without requiring ongoing access to sensitive transaction data. This approach satisfies regulatory requirements like NACHA's Web Debit Account Validation Rule while avoiding the fee structures that banks are implementing for broader data access.

GrailPay’s Account Intelligence model offers secure, real-time onboarding without the costs of open banking

The industry appears to be moving toward a more purposeful use of open banking, where companies reserve comprehensive data access for specific use cases that truly require transaction histories and detailed financial insights – such as cash flow underwriting, income verification, or personal financial management tools.

For standard payment processing, credentialless account validation technology offers a more cost-effective and focused solution. As banks continue to monetize their data and regulatory frameworks remain in flux, companies that can achieve their core payment objectives without extensive open banking dependencies will find themselves in a stronger competitive position.

The key is matching the right tool to the specific business need rather than defaulting to the most comprehensive data access available. In an environment where data access costs are rising and regulatory certainty is declining, this focused approach isn't just financially prudent – it's strategically essential.

Looking for an account validation solution? Get in touch!

.svg)

.svg)