.svg)

.svg)

GrailPay's 2025 year in review

The last year was a whirlwind of building, shipping, learning, and proving what's possible when you rethink how bank payments work from the bottom up.

As we step into 2026, we wanted to take a moment to reflect on how far GrailPay has come, and share what we're most excited for this year.

Looking back: payments is the plumbing of B2B commerce

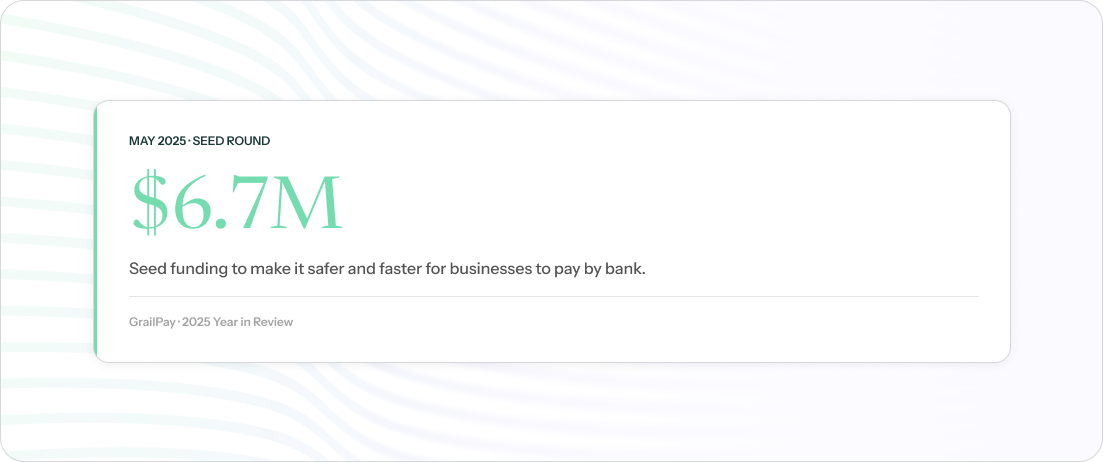

2025 marked a major turning point for GrailPay. In May, we announced our $6.7M seed funding round, giving us the resources to accelerate our mission: making it safer and faster for businesses to pay by bank.

At any given moment during the workweek, about a trillion dollars of B2B bank payments are in transit. That's operating capital locked up and unavailable for product development, growth investments, dealmaking, or even just making payroll. A trillion dollars of daily economic potential, held hostage by infrastructure that's nearly half a century old.

We think that's insane. And more importantly, we think it's fixable.

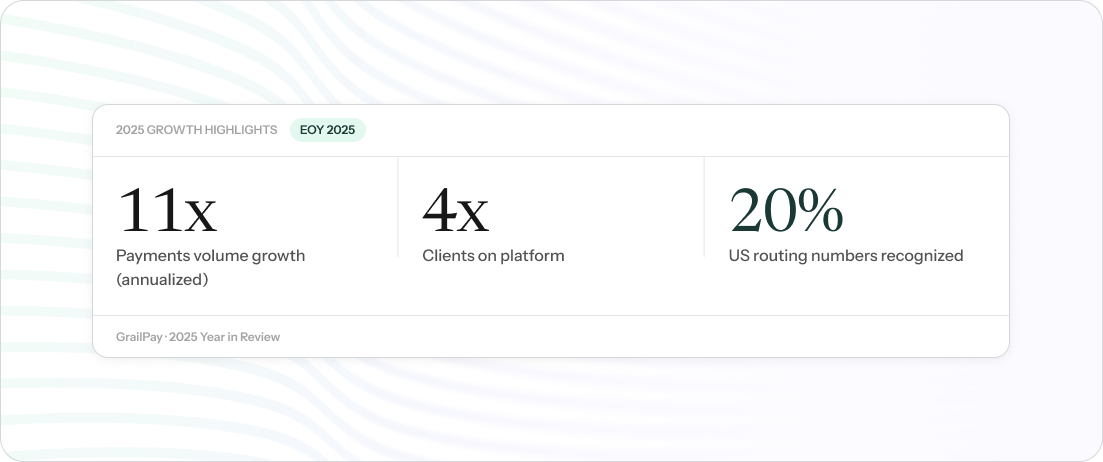

And, in getting to work on the fix, we’ve hit some big numbers this year:

- Grew payments volume 11x% to $B annualized EOY 2025

- 4x'd clients on platform

- Recognized and cataloged over 20% of US routing numbers

The numbers are just half the story, as the real progress happened on platform.

Account Intelligence: the new standard for bank account validation

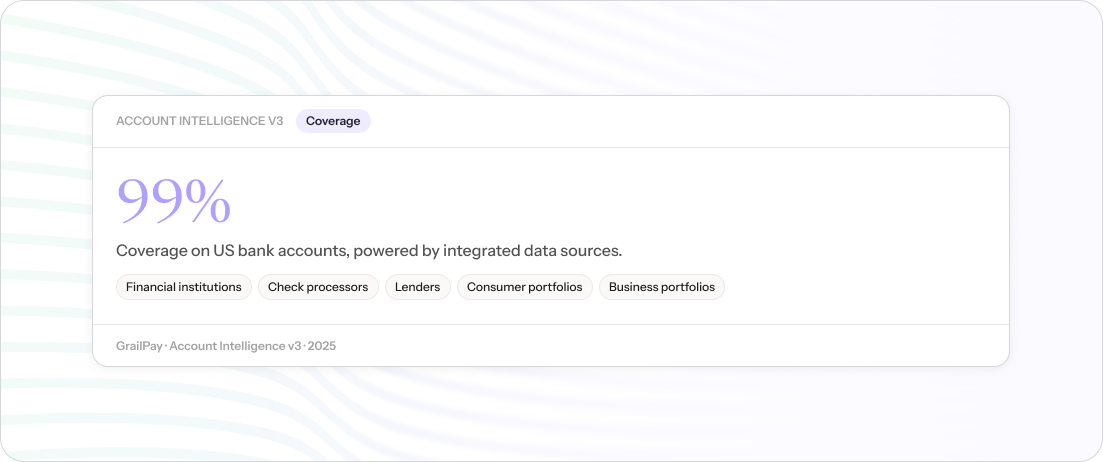

In Q2 we launched our third version of our flagship risk model, Account Intelligence. It’s our most powerful release yet. By integrating new data sources like check processors, lenders, and financial institutions with consumer and business portfolios, we now achieve 99% coverage on US bank accounts.

As part of v3 we also shipped our name match capability, allowing our clients to verify that the name on a bank account matches the user going through their onboarding or payments flow. It's a simple concept, but it closes a significant gap that bad actors have exploited for years.

FedNow Send: settlement in seconds

We rolled out our first instant payments capability with FedNow Send, letting clients make real-time payouts and cut settlement from days to under 20 seconds. We’ll be adding even more instant rails soon, with intelligent routing for cost and success rate faceted in by design.

Looking forward: B2B is going instant, on-chain, and agentic, and that comes with a new bar for risk

Heading into 2026, we're focused on three trends that will define the next era of business payments: guaranteed instant settlement, stablecoin adoption, and agentic commerce.

Here's the paradox of legacy ACH: the slow settlement is annoying and locks up capital, but it's also load-bearing. The extra time gives the system room to catch bad payments and allows for communication of return codes and manual reviews. The system was originally designed for most of that to happen in the gap between initiation and settlement, so the delay is a feature, not a bug.

We think that's a bad trade-off. A trillion dollars in limbo at any given moment is too high a price to pay for safety-by-slowness. But we can't just rip out the delay and hope for the best. Faster settlement without better risk infrastructure isn't progress, it's just faster losses.

So, we're building the trust layer that finally lets businesses safely speed money up with a real-time, preemptive risk assessment that answers the hard questions - who is this, can they pay, and should we trust them? - before payments process, not after.

Here's where it gets interesting: the bar you have to clear to de-risk instant payments is the same bar required for stablecoins and agentic commerce. All three remove the safety nets that traditional payments rely on. Instant settlement eliminates the time buffer. Stablecoins remove the banking intermediaries. Agentic commerce removes the human in the loop. In every case, you need a zero-trust, always-verify approach to risk, assessing identity, capability, and intent upfront, portable across every interaction.

That's what we're building. One risk layer that works across legacy ACH, new instant rails, and on-chain payments. The connective tissue that makes the future of B2B payments actually viable, gated behind user-authenicated trust.

Thank you

To our clients, partners, advocates, and investors; thank you for believing in what we're building.

2025 proved that better bank payments are possible. 2026 is where we go from better to best and rewrite the standard.

Here's to a challenging, exciting year ahead.

.svg)

.svg)